To increase access to affordable health care, health insurers are bringing new plan options and tools to the market to help curb costs.

A plan tied to a health savings account (HSA) or a narrow network health plan associated with one health system are two options that can save you money. You might be surprised by the cost savings these health plans can provide to you and your family. Explore your options during this year’s Open Enrollment Period, which runs from Nov. 1 to Dec. 15, 2017.

We answered some questions below to help you decide if one of these options is right for you and your family.

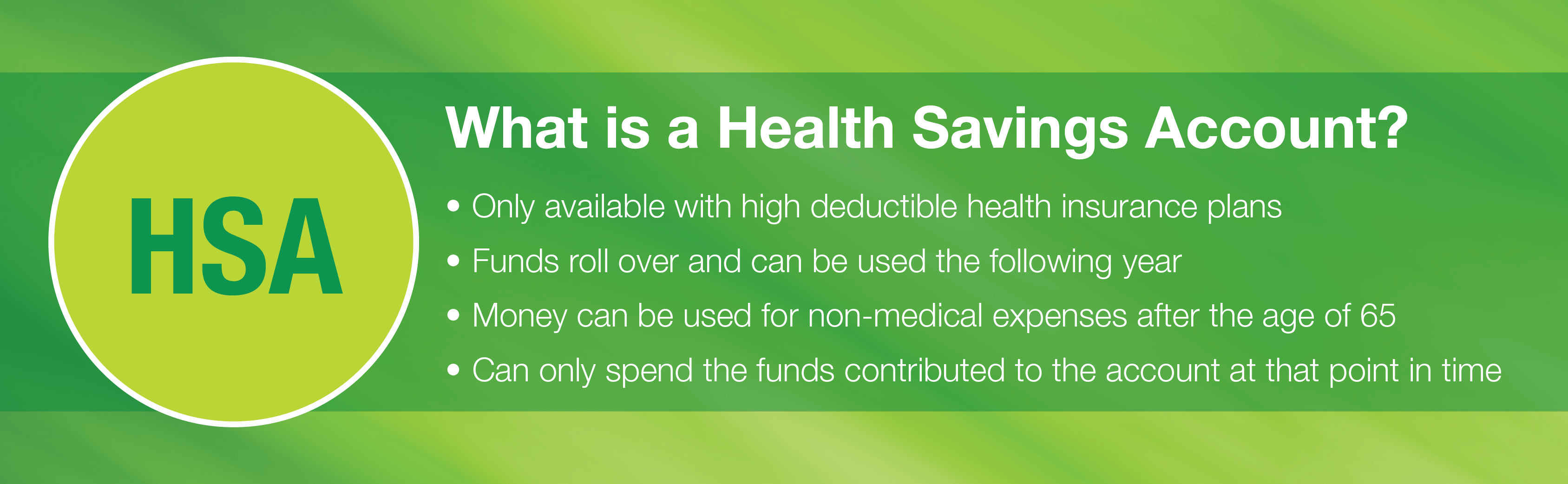

What is an HSA?

An HSA is a savings account paired with a high-deductible health insurance plan. You contribute money to your HSA like you would with any savings account, but this account can only be used to pay for health care expenses. This model helps you plan for, and save money on, any out-of-pocket health expenses such as copays, coinsurance or your deductible.

One of the biggest advantages to using an HSA is that you can save money tax free. This means that any contributions you make to the savings account are not taxed and the balance grows tax-free. Similarly, withdrawals are not taxed as long as they are used for qualified medical expenses.

Another benefit is that any money that goes unused rolls over into the following year, helping you build your health savings account over time.

All funds in your HSA account belong to you as the account owner, meaning it travels with you from one job to another, and into retirement. If you don’t need to make large withdrawals from this account for health care expenses, an HSA is also a great retirement planning tool. Once you turn 65, you can use the money for non-medical related expenses without a penalty.

Is an HSA right for me?

If you are generally healthy and savings-minded, and don’t anticipate needing major medical care, an HSA may be the right choice for you. HSAs may also benefit those people nearing retirement as they are an excellent way to offset costs after retirement.

What is a narrow network?

The term network refers to providers or health care facilities that are a part of a health plan. It is most cost effective if you visit in-network doctors and facilities because your health insurer has already negotiated a discounted rate for health care services.

Health insurance plans paired with narrow networks typically offer a lower monthly premium and require members to receive care within one health system. Care received outside of the health system’s network is generally not covered and members are required to cover the full cost of out-of-network care.

Is a narrow network right for me?

If you receive care from one health system (or are comfortable with that approach) and are interested in a lower monthly premium, a narrow network plan could be a great way to manage your health care spending. The lower premiums balance out the limited network – especially if you only visit your doctor for routine checkups and don’t require many prescriptions or medical testing. Make sure your preferred providers are within the network before receiving care.

This Open Enrollment Period be sure to look into how contributing to a health savings account or enrolling in a narrow network plan could help you manage your health care expenses and take control of your health care spending.