For many Americans, it is a challenge to keep up with the out-of-pocket expenses that have become synonymous with staying healthy.

A health spending account can help you manage these expenses and save money in the long run.There are two versions that act similar to personal savings accounts, set aside especially for your medical expenses – a health savings account (HSA) and a flexible spending account (FSA).

Regardless of the account you use, you own and control the money within it. It even moves with you if you leave your job. Best of all, any money that you contribute to the account is tax-exempt. This means that you could see significant savings by paying for your health expenses pre-tax using the health spending account.

Often health savings account options are coupled with the plan you choose through your employer, but you may need to seek one out if you shop for a plan on your own. Either way, they are a great tool for budgeting and saving on health care expenses and are definitely worth exploring.

But what’s the difference between an HSA and an FSA?

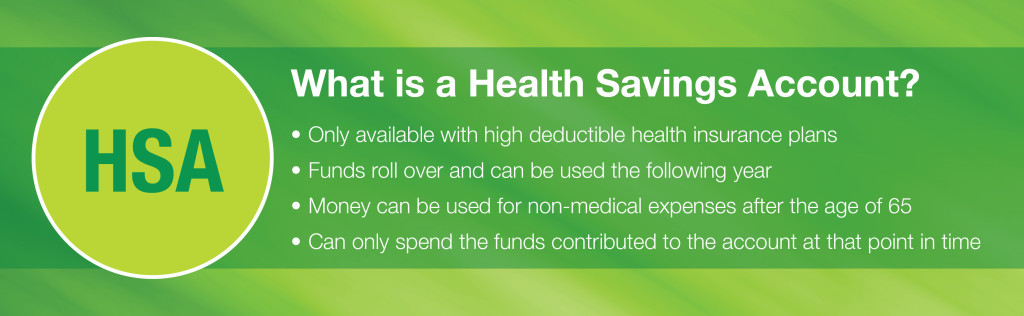

HSA:

While an HSA is only available with a high deductible insurance plan, it affords a little bit more flexibility. If you don’t spend all the money in your HSA by the end of a calendar year, the funds roll over and can be used the following year. Plus, after you turn 65, you can use the money in your account for non-medical expenses without a penalty. An HSA only allows you access to the funds you have already contributed at that point in time.

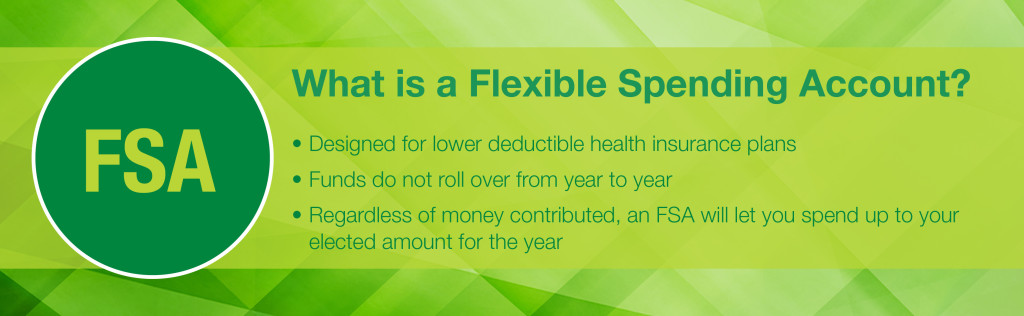

FSA:

An FSA offers the same savings and pre-tax benefits as an HSA, but can be used with any type of health plan. The main difference between an HSA and an FSA, is that with an FSA, the funds don’t roll over, therefore you can’t, and probably don’t want to, contribute as much money toward it each year. It is a use-it or lose-it type of account. However, an FSA will let you spend up to your elected amount for the year, at any time, regardless of whether you’ve completed your contributions.

Both types of health spending accounts will pay off when it comes to your taxes, though.

After determining which types of health spending accounts are offered as a part of your health plan, the next step is to better understand your expenses and define your ideal contribution for the year. Sometimes you employer will even contribute to your account. Not only does the health spending account help you save for future health care expenses, it helps you budget by planning ahead based on past health care expenses.

The expenses that qualify are determined by government regulations and include:

- Co-pays for medical expenses and drugs

- Doctor and hospital visits, including surgeries

- Prescription drugs (over-the-counter medications are not covered without a prescription)

- X-rays and lab tests

- Dental and orthodontia expenses

- Vision expenses

- Medical equipment, such as wheelchairs

There is a 20 percent penalty for using a HSA or FSA for non-qualified expenses, so it’s important to make sure your expenses qualify to avoid any penalties. For both accounts, it’s a good idea to always keep all of your health care service receipts and payment notifications for reference. Both types of accounts are easy to use and often come with a debit card to pay for health expenses on the spot with no additional paperwork.

Contributing to a health spending account allows you to save money and to have more control and flexibility over where your health care dollars go. Whether you have an HSA or an FSA, these tax-exempt accounts will help you better navigate your health care expenses.