Whether you get health insurance through your employer or you buy coverage for yourself, choosing the right plan is challenging. Your decision impacts your finances and your health, so it’s worth doing some research.

In general, the amount you pay is tied to your freedom to choose where you get care. The more flexibility you want, the more you’ll pay. But if you’re willing to limit your choice, you could save money.

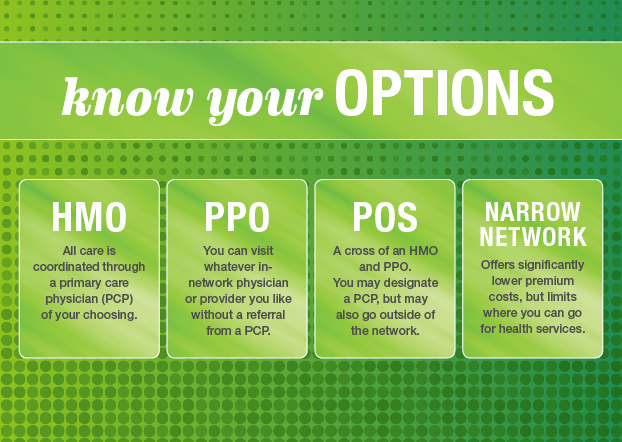

Here’s what you should know about today’s most popular kinds of health insurance before deciding what’s best for you and your family:

What is an HMO? – More than 3 million Michigan residents have an HMO plan, and it’s easy to see why they’re so popular. HMOs, also called health maintenance organizations, were introduced in the 1970s as a way to keep health care costs under control. If you want to keep your costs down and get reliable care, an HMO may be your best choice.

- How it works: You’ll need to choose a primary care provider and you’ll be able to use doctors and hospitals that are part of a large network. Often, you can even see in-network specialists without a referral. But keep in mind that you won’t be covered for out-of-network services unless it’s a medical emergency.

- Insider tip: Before choosing a plan, research the HMO’s network. If your favorite doctors and hospitals are included, you’re good to go.

What is a PPO? – You’ll have more freedom of choice with a PPO plan, which is also called a preferred provider organization. If flexibility is most important to you, and you can afford higher premiums and out-of-pocket costs, a PPO may be your best choice.

- How it works: The amount you pay for services will depend on whether you use in-network or out-of-network providers. You’ll have the option of going outside of the network by paying extra for services. The choice is yours.

- Insider tip: You’ll save money by using doctors and hospitals in your PPO network. Only go out of your PPO network for specialized care or major health concerns.

What is POS? – A point of service, or POS plan, is a cross between an HMO and a PPO. You’ll have two payment levels (called benefit levels) depending on whether you receive your care in or out of your provider network.

- How it works: A POS gives you the best of both worlds. It encourages you to use a primary care provider to coordinate your care but you can also get out-of-network care when needed.

- Insider tip: To save money, be sure to choose an in-network primary care provider (even if your insurance company doesn’t require it.) If you don’t have one, the higher payment schedule applies—even when you use in-network specialists.

What is a Narrow Network? – Plans with narrow networks are growing in popularity because they have significantly lower premiums. The tradeoff: You’ll have limits on where you can go for health care services. If you can live with fewer choices (or better yet, you already see an in-network doctor) and you want to keep your premium costs down, this might be a great option for you.

- How it works: Narrow network plans are based on agreements between a health insurance company and a hospital system or specific doctors. Buyer beware: If a doctor, lab or hospital isn’t in the network, you’ll be responsible for paying 100 percent of the cost except in the case of a medical emergency.

- Insider tip: Understand exactly where you can (and cannot) go for care, and check the quality information for the hospitals and doctors in the plan. Some narrow networks use major, regional healthcare systems with enough well-respected hospitals and doctors to meet your needs.